The Social Cost of Kerala’s Fiscal Crisis: When SC/ST Development Spending Becomes a Budgetary Casualty

Kerala’s fiscal crisis is usually discussed in terms of debt, deficit and KIIFB liabilities. But the White Paper reveals a deeper social concern: development spending meant for Scheduled Castes and Scheduled Tribes has been sharply compressed. The share of Plan expenditure on SC/ST/OBC and minority welfare fell from 9.24 per cent in 2017–18 to 3.85 per cent in 2025–26 (RE), while SCSP and TSP together recorded a cumulative shortfall of over Rs 7,257 crore during 2017–18 to 2024–25. KIIFB did not compensate for this decline. This article by Prof. A M Jose and Prof. Jos Chathukulam argues that Kerala’s fiscal crisis must be judged not only by financial indicators, but also by its social cost: whose development is protected, and whose development is postponed.

Introduction

Kerala’s 2026 White Paper on fiscal health has already generated serious discussion on debt, deficits, KIIFB, public sector enterprises, treasury stress and Centre–State fiscal relations. These are important issues. But hidden within the larger fiscal debate is another question that deserves urgent public attention: what has happened to Kerala’s development spending for Scheduled Castes and Scheduled Tribes?

This is not a minor accounting issue. It goes to the heart of the Kerala model. Kerala’s development reputation was built not merely on aggregate literacy, health or welfare indicators, but on the promise that public action would reduce social exclusion and expand opportunities for historically disadvantaged groups. If fiscal stress weakens this commitment, then the crisis is not only financial. It becomes a social justice crisis.

The Scheduled Caste Sub Plan (SCSP) and Tribal Sub Plan (TSP) are not ordinary welfare items in the budget. They are instruments of targeted development. Their purpose is to ensure that Scheduled Castes and Scheduled Tribes receive a fair and proportionate share of development expenditure. In Kerala’s planning framework, 9.81 per cent of the State Plan outlay is earmarked for SCSP and 2.83 per cent for TSP. Together, this comes to 12.64 per cent of the State Plan outlay.

The principle is simple. Communities that have faced historical deprivation cannot be left to depend only on general development expenditure. They require targeted public investment in education, housing, health, livelihoods, local infrastructure, land-related support and social protection. This is also consistent with Article 46 of the Constitution of India, which directs the State to promote with special care the educational and economic interests of Scheduled Castes and Scheduled Tribes and protect them from social injustice and exploitation.

The White Paper’s evidence is therefore deeply worrying. It shows that the share of Plan expenditure on the welfare of SC/ST/OBC and minorities declined from 9.24 per cent in 2017–18 to only 3.85 per cent in 2025–26 (Revised Estimate). This broader category includes not only SCs and STs but also OBCs and minorities. Yet even this wider welfare category is far below the combined SCSP and TSP benchmark of 12.64 per cent.

This means that the problem is not only underperformance in one scheme or one department. It points to a broader weakening of social justice expenditure within Kerala’s Plan spending.

The Declining Share of Welfare Expenditure

The White Paper shows a clear downward trend. In 2017–18, welfare expenditure for SC/ST/OBC and minorities was 9.24 per cent of total Plan expenditure. By 2025–26, it had fallen to 3.85 per cent. In relation to the 12.64 per cent SCSP+TSP benchmark, this means that the actual share declined from about 73 per cent of the benchmark to just about 30 per cent.

Table 1: Plan Expenditure on Welfare of SC/ST/OBC and Minorities: A Benchmark Comparison with the SCSP+TSP Norm

| Year | Actual share of total Plan expenditure (%) | Gap from 12.64 % norm (percentage points) | Actual as share of 12.64 % norm (%) |

| 2017-18 | 9.24 | 3.40 | 73.10 |

| 2018-19 | 9.52 | 3.12 | 75.32 |

| 2019-20 | 7.05 | 5.59 | 55.78 |

| 2020-21 | 6.87 | 5.77 | 54.35 |

| 2021-22 | 6.04 | 6.60 | 47.78 |

| 2022-23 | 6.01 | 6.63 | 47.55 |

| 2023-24 | 5.68 | 6.96 | 44.94 |

| 2024-25 | 5.28 | 7.36 | 41.77 |

| 2025-26 (RE) | 3.85 | 8.79 | 30.46 |

Source: Calculated by the authors from Government of Kerala (2026), Table 6.5. Note: The actual share refers to the broader category SC/ST/OBC/minorities; the 12.64 per cent benchmark is the combined planning norm for SCSP and TSP.

Table 1 needs to be read carefully. It does not mean that SCSP and TSP alone received 3.85 per cent. The White Paper’s category is broader. But that is precisely why the figure is disturbing. If the broader category covering SC/ST/OBC and minorities itself falls to 3.85 per cent, then the priority given to targeted welfare in the Plan has clearly weakened.

This is where fiscal stress becomes socially unequal. A government may face shortage of money. But when money becomes short, which expenditure is protected and which expenditure is postponed? That is the real question.

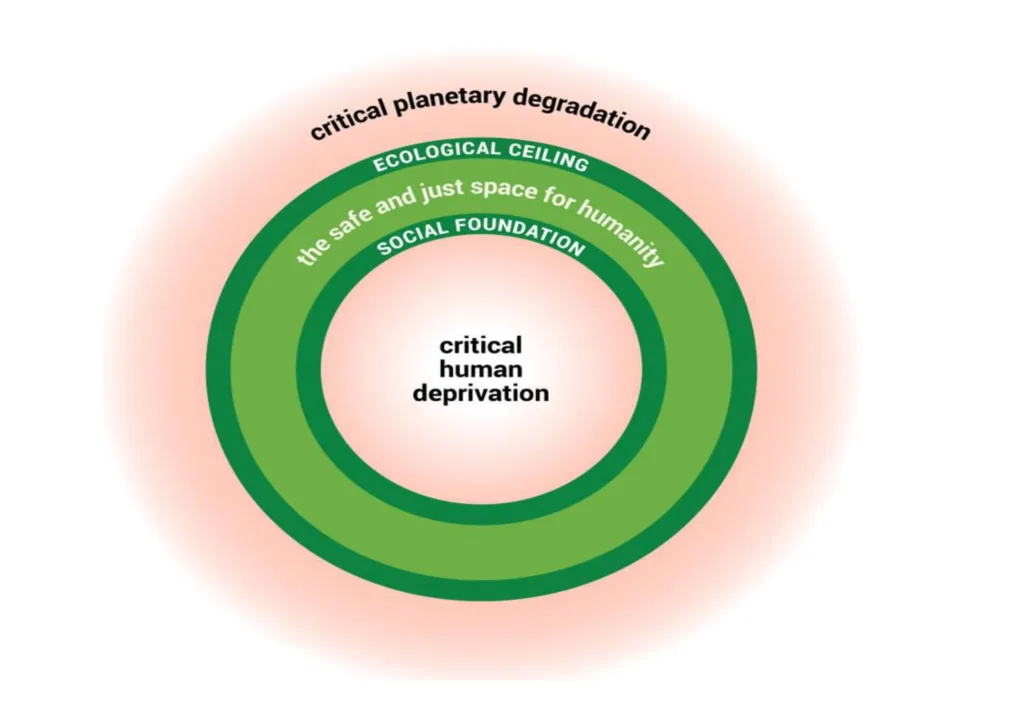

This can also be read through the lens of Doughnut Economics. Raworth’s framework defines development as the creation of a “safe and just space” between the social foundation and the ecological ceiling. In the present context, the sharp fall in targeted welfare expenditure suggests a shortfall in Kerala’s social foundation for SC and ST communities. When the broader SC/ST/OBC/minority welfare share falls to 3.85 per cent against the 12.64 per cent SCSP+TSP benchmark, and when SCSP and TSP together show a cumulative shortfall of over Rs 7,257 crore, the problem is not only fiscal compression; it is a movement away from the safe and just space that inclusive development requires.

Figure 1: Doughnut Economics: The Safe and Just Space

Source: Raworth, K. (2025). The evolving doughnut. Doughnut Economics Action Lab. https://doughnuteconomics.org/tools/the-evolving-doughnut

In this article, the Doughnut framework is used only as an interpretive lens: the shortfall in SCSP and TSP expenditure is read as a shortfall in Kerala’s social foundation for SC and ST communities.

Outlay Is Not Enough: The Problem of Utilisation

Allocating money is only the first step. The money must also be spent effectively and on time. Here too, the White Paper raises serious concerns.

Between 2017–18 and 2024–25, total SCSP outlay was Rs 22,817.39 crore. Actual expenditure was Rs 17,864.97 crore. The cumulative shortfall was therefore Rs 4,952.42 crore. In 2019–20, SCSP utilisation fell sharply to 49.60 per cent. Even in better years, full utilisation was not achieved.

The TSP picture is also worrying. Between 2017–18 and 2024–25, total TSP outlay was Rs 7,354.60 crore. Actual expenditure was Rs 5,049.99 crore. The cumulative shortfall was Rs 2,304.61 crore. Utilisation fell to 55.68 per cent in 2019–20 and again to 56.29 per cent in 2023–24.

Taken together, the cumulative shortfall in SCSP and TSP expenditure during 2017–18 to 2024–25 was more than Rs 7,257 crore. This is not a small year-end adjustment. It represents a major loss of development opportunity for communities that require sustained public investment.

A shortfall in SCSP may mean delays in housing, scholarships, skill development, local infrastructure, livelihood schemes or educational support. A shortfall in TSP can be even more damaging because tribal development is linked to land, forest rights, nutrition, residential schooling, health access, drinking water, roads and protection from displacement. In many tribal regions, public expenditure is not just support; it is often the main bridge between constitutional promise and actual development.

Did KIIFB Compensate? The Evidence Says No

One possible argument is that even if conventional Plan expenditure declined, KIIFB may have compensated through infrastructure investment. KIIFB was created as a special infrastructure financing mechanism to overcome budgetary constraints and accelerate capital investment. If KIIFB had incorporated strong social justice criteria into project selection, it could have partly offset the decline in targeted Plan spending.

But the White Paper shows that this did not happen.

The Scheduled Castes Development Department received KIIFB project approvals of only Rs 92 crore. The White Paper reports this as 0.07 per cent of total approvals. Recalculation from the total KIIFB approved amount of Rs 1,19,412.47 crore gives 0.077 per cent, which rounds to 0.08 per cent. Payments released to the Scheduled Castes Development Department were Rs 64 crore, or 0.07 per cent of total payments released.

The Scheduled Tribes Development Department received approvals of only Rs 49 crore, or 0.04 per cent of total approvals. Payments released were Rs 18 crore, or 0.02 per cent of total payments released.

Table 2: KIIFB Approvals and Payments for SC and ST Departments

| Department | Approved amount (Rs crore) | Share of total approvals (%) | Payment released (Rs crore) | Share of total releases (%) |

| Scheduled Castes Development Department | 92 | 0.08 | 64 | 0.07 |

| Scheduled Tribes Development Department | 49 | 0.04 | 18 | 0.02 |

Note: The White Paper text reports the SCDD’s approved share as 0.07 per cent. Recalculation from the total approved amount of ₹1,19,412.47 crore gives 0.077 per cent, which rounds to 0.08 per cent.

Source: Calculated by the authors from Government of Kerala (2026), Chapter 6, using total KIIFB approved amount and payment released reported in Table 4.6.

These are not compensatory flows. They show that KIIFB did not function as a corrective mechanism for the weakening of targeted Plan expenditure. This is important because KIIFB represents a development strategy in which large infrastructure projects are financed through a parallel mechanism. If such a mechanism does not carry explicit social inclusion obligations, the distributive discipline of planning is weakened.

Infrastructure is important. Roads, bridges, hospitals, schools and public buildings matter. But infrastructure does not automatically become social justice. The key questions are: where are these projects located? Who benefits most? Do they address areas of historical deprivation? Do they improve the lives of Scheduled Castes and Scheduled Tribes in measurable ways? Are social justice criteria built into project appraisal?

Without such questions, infrastructure-led development can bypass the very communities that need public investment the most.

Fiscal Stress Is Real, But So Is Social Priority

Kerala’s fiscal stress is real. High committed expenditure, debt servicing, pension obligations, treasury pressures, weak capital expenditure and Centre–State fiscal constraints cannot be ignored. A responsible public debate must acknowledge these realities.

But fiscal stress cannot become an excuse for making social justice expenditure residual. The SCSP and TSP were created precisely to prevent this. Their purpose is to ensure that the claims of historically marginalised communities do not disappear when the budget becomes tight.

The White Paper makes an important observation: SCSP and TSP expenditure fell short even in years when aggregate expenditure exceeded total outlay. This means the problem cannot be explained only by shortage of money. It also reflects prioritisation, administrative capacity, timing of releases, project readiness and the political visibility of different expenditure heads.

Committed expenditure such as salaries, pensions and interest payments is difficult to compress. Large infrastructure projects often acquire political visibility and contractual force. But targeted social development schemes depend on administrative follow-up, beneficiary identification, local government capacity, departmental coordination and timely release of funds. When fiscal stress appears, these schemes can be postponed with less immediate political cost. But the social cost is borne by communities with weaker voice in budgetary politics.

This is why the issue must be discussed publicly in Kerala. The question is not whether Kerala should be fiscally responsible. It must be. The question is whether fiscal responsibility will be pursued in a socially responsible way.

What Should Kerala Do?

First, SCSP and TSP allocations should be treated as non-divertible commitments. If expenditure falls below the mandated share, the government should be required to explain the reasons publicly before the legislature and indicate how the shortfall will be restored.

With the forthcoming Budget scheduled for the 19th, this issue should be placed before the government as a clear budget proposal: the cumulative shortfall in SCSP and TSP expenditure must be recognised and progressively compensated. The Budget should not merely restore the annual 9.81 per cent SCSP and 2.83 per cent TSP norms; it should also announce a credible roadmap to make good the development opportunity losses suffered by SC and ST communities during the years of underutilisation.

Second, Kerala should publish a clear SCSP–TSP Budget Statement every year. This statement should show outlay, release, actual expenditure, physical targets, outcomes and district distribution. It should not merely list schemes; it should show whether the 9.81 per cent and 2.83 per cent norms are being met in substance.

Third, unspent SCSP and TSP funds should be tracked through a restoration mechanism. When funds remain unspent, they should not simply disappear into the next budget cycle. The cumulative shortfall must be recognised as an opportunity loss and corrected over time.

Fourth, KIIFB and any future infrastructure financing mechanism should include mandatory social inclusion criteria. A fixed equity window for SC and ST development, district deprivation weights and social impact appraisal can help ensure that infrastructure finance does not bypass marginalised communities.

Fifth, local governments must be strengthened to implement SCSP and TSP projects. Kerala’s decentralised planning tradition is one of its major democratic assets. But devolution without technical support, timely fund release and social audit will not deliver justice. SC and ST communities must have a stronger voice in project choice and monitoring.

Sixth, Kerala should move beyond financial audit to outcome audit. It is not enough to ask whether money was spent. The real question is whether housing improved, school retention increased, health access expanded, drinking water reached settlements, livelihoods improved and local infrastructure strengthened in SC and ST habitations.

Finally, the legislature should receive an annual Social Justice Expenditure Report. Such a report should compare mandated outlay, actual expenditure, cumulative shortfall, KIIFB and other agency spending, district spread and measurable outcomes. This would convert constitutional commitment into budgetary accountability.

Conclusion

Kerala does not have to choose between fiscal responsibility and social justice. It must choose both. Fiscal discipline is necessary. But a fiscally responsible state cannot become socially irresponsible.

The evidence from the White Paper tells a clear story. The broader welfare share for SC/ST/OBC and minorities declined from 9.24 per cent to 3.85 per cent. SCSP and TSP together saw a cumulative shortfall of more than Rs 7,257 crore during 2017–18 to 2024–25. KIIFB did not compensate for this decline. These facts raise a fundamental question: when money becomes scarce, whose development is protected and whose development is postponed?

The answer to that question will decide the future of the Kerala model. If social justice becomes residual, the Kerala model will survive only as an aggregate achievement, not as a living project of social transformation. But if Kerala uses the White Paper as an opportunity to protect targeted development spending, strengthen local governments, reform KIIFB and make public finance more accountable, the state can rebuild its fiscal foundations without abandoning its social commitments.

Kerala’s fiscal crisis must therefore be debated not only in terms of debt and deficit, but also in terms of dignity, justice and democratic accountability.

Selected References

Chathukulam, J., Reddy, M. G., & Rao, P. T. (2012). An assessment and analysis of Tribal Sub Plan (TSP) in Kerala. Centre for Economic and Social Studies.

Chathukulam, J. (2026). Integrating Doughnut Economics into People’s Planning: A Sustainable Development Paradigm for Kerala and Beyond. Indian Public Policy Review, 7(2), 44-55. [1, 2]

Drèze, J., & Sen, A. (2013). An uncertain glory: India and its contradictions. Princeton University Press.

Government of India. (1950/2024). The Constitution of India. Ministry of Law and Justice, Legislative Department.

Government of Kerala. (2026). Kerala’s fiscal health: A status report. Finance Department, Government of Kerala.

Isaac, T. M. Thomas, & Franke, R. W. (2000). Local democracy and development: People’s Campaign for decentralized planning in Kerala. LeftWord Books.

Raworth, K. (2017). Doughnut economics: Seven ways to think like a 21st-century economist. Random House Business.

Jos Chathukulam is a Professor of Political Economy and Director of the Centre for Rural Management (CRM), Kottayam, Kerala. His academic work focuses on public policy, decentralisation, public finance, local governance, development studies, and political economy in India, with a special emphasis on Kerala. Prof. Chathukulam has authored and edited several influential books and research papers, and has served as a policy advisor to governments and international agencies. He is widely recognised for his critical engagement with development paradigms and for advocating sustainable, people-centred alternatives in economic and governance practices.