Kerala’s White Paper Moment: Fiscal Truth, Democratic Accountability and the Search for a New Public Finance Compact

Kerala’s 2026 White Paper on fiscal health is an important attempt to place the state’s finances before the public with greater transparency. But White Papers do not by themselves correct fiscal crises; they create a baseline for democratic accountability and reform. This article by A M Jose and Jos Chathukulam places the 2026 White Paper within the larger history of White Papers, Kerala’s earlier fiscal diagnoses, and K. K. George’s 1990 argument that Kerala’s fiscal crisis is structural rather than temporary. It argues that Kerala’s repeated White Papers show the persistence of the same underlying fiscal contradictions: high committed expenditure, weak capital formation, off-budget liabilities, public enterprise losses, constrained fiscal federalism and insufficient revenue mobilisation. The challenge is not merely to expose the crisis, but to build a fiscally responsible and developmentally just reform programme.

What is a White Paper? History, Rationale and World Experience

A White Paper belongs to the parliamentary tradition of public policy disclosure. Historically, it evolved in the British system as a formal government document used to place a considered policy position before Parliament and the public. Unlike a routine budget speech or a party manifesto, a White Paper is expected to present the government’s diagnosis of a serious policy issue, justify the need for reform and create a basis for informed debate. In many parliamentary systems, White Papers have been used to announce future legislative proposals, defence reforms, constitutional changes, fiscal strategies, welfare reforms and institutional restructuring.

The democratic rationale of a White Paper lies in three ideas: transparency, accountability and public reasoning. First, it places facts before the legislature and citizens. Second, it creates a baseline against which the future performance of the government can be judged. Third, it prepares citizens for difficult choices. A White Paper is therefore not merely a technical document; it is a political economy document. It tells us not only what the government knows, but how it interprets the problem and what kind of reform it considers legitimate.

In fiscal policy, the importance of a White Paper is even greater. Ordinary budgets often focus on annual receipts and expenditure. But fiscal stress is rarely confined to one year. It hides in deferred payments, off-budget borrowings, guarantees, loss-making public enterprises, unpaid dues, pension burdens, contingent liabilities and weak revenue mobilisation. A serious fiscal White Paper should therefore reveal not only the budget deficit, but the state’s true fiscal position.

In parliamentary democracies and public finance practice, White Papers and similar fiscal status reports have generally served as instruments of disclosure, public reasoning and reform preparation. World experience shows that White Papers can perform different roles. In Britain and other Westminster systems, they have often been used to move from policy diagnosis to legislation. In Canada, Australia and New Zealand, similar policy papers have helped governments create public debate around fiscal reform, social policy and public expenditure priorities. In development policy, governments and international institutions also use status reports, public expenditure reviews and fiscal responsibility statements to diagnose fiscal weaknesses and propose institutional reforms. The common lesson is clear: a White Paper can improve fiscal governance only when it is followed by credible institutional action—legislation, fiscal rules, public expenditure reviews, budget transparency reforms or parliamentary monitoring. Where it remains only a diagnostic document, it may improve public debate but will not by itself alter fiscal behaviour.

This is where the limitation begins. A White Paper can expose a problem, but it cannot solve it. It can create transparency, but not discipline. It can diagnose fiscal weakness, but not automatically generate political courage. Its success depends on what follows: revenue reform, expenditure restructuring, better budgeting, transparent treatment of liabilities, public enterprise reform and protection of productive capital expenditure.

Kerala’s 2026 White Paper must be read in this light. It should not be treated merely as a document of blame. Nor should it be accepted uncritically as a complete reform blueprint. It should be understood as a moment of fiscal truth: an opportunity to ask whether Kerala can combine welfare, growth, public investment and fiscal responsibility in a new public finance compact.

This article therefore addresses a central question: why have repeated White Papers and fiscal diagnoses in Kerala failed to produce lasting fiscal correction, and how can the 2026 White Paper be converted into a democratic, development-oriented public finance reform agenda? The answer lies not merely in better accounting, but in translating fiscal transparency into institutional reform, productive public investment, social justice and political consensus.

Kerala’s History of White Papers: Diagnosis Without Structural Correction?

Kerala has had four major official fiscal disclosure exercises, including White Papers or equivalent status-report moments: 2001, 2011, 2016 and 2026. In addition, opposition parties have occasionally issued their own “white papers,” but these must be distinguished from official government documents. Each of the four official exercises emerged after a change in government or a moment of political-fiscal contestation. Each claimed to reveal the true state of Kerala’s finances. Each diagnosed fiscal stress. Yet the recurrence of White Papers itself tells us something important: earlier diagnoses did not produce lasting structural correction.

The 2001 White Paper, brought out after the UDF government assumed office under A. K. Antony, projected the state’s finances as severely depleted. Its political message was clear: the new government had inherited an empty treasury and a serious fiscal crisis. The 2011 White Paper, again under a UDF government, explicitly referred to the 2001 White Paper and focused on the decade from 2001–02 to 2010–11. It sought to present the facts about the financial position of the state and to initiate wider debate on economic recovery and fiscal consolidation. Its very framing shows that the problems identified in 2001 had not disappeared.

The 2016 White Paper, presented by the LDF government under Finance Minister T. M. Thomas Isaac, again described Kerala’s fiscal position as alarming. It pointed to negative treasury balances, rising liabilities, weak revenue mobilisation, neglect of deficit targets and lack of funds for capital expenditure. This was also the period in which KIIFB was restructured as a major development-finance instrument to overcome the state’s chronic capital-expenditure constraint. The logic was understandable: if the ordinary budget could not provide enough capital expenditure, a special infrastructure financing vehicle could front-load investment. But as later developments showed, off-budget borrowing did not eliminate fiscal obligations; it merely changed their institutional form.

The 2026 White Paper appears after another political transition and after a decade of intensified fiscal stress. It is the most comprehensive of the four in scope. It includes not only budgetary debt and deficits, but also off-budget liabilities, KIIFB, KSSPL, public sector enterprises, treasury stress, arrears, local government finance, development expenditure and Centre–State fiscal relations. In that sense, it has a wider fiscal boundary than earlier exercises.

The larger question is whether any of the previous White Papers improved Kerala’s fiscal situation. The answer must be nuanced. They improved transparency for a time. They made fiscal stress a matter of public debate. They forced governments to acknowledge liabilities and budgetary constraints. But they did not lead to durable structural correction.

Why? Because the drivers of Kerala’s fiscal crisis remained largely intact. Revenue expenditure continued to dominate total expenditure. Salaries, pensions and interest payments remained high. Own revenue mobilisation did not keep pace with expenditure commitments. Capital expenditure remained modest. Public sector losses continued. Fiscal federal constraints became tighter after GST and the end of compensation. Off-budget mechanisms such as KIIFB and KSSPL emerged to bypass fiscal limits, but eventually became part of the state’s effective liability structure.

This is precisely the point made in our earlier analysis of Kerala’s fiscal crisis across three and a half decades. K. K. George’s 1990 diagnosis was that Kerala’s fiscal crisis was structural: current-account stress, heavy debt servicing, pension commitments, the revenue-heavy nature of social expenditure and limited space for developmental outlay. More than three decades later, the vocabulary has changed, but the structure remains. The old non-plan revenue gap has reappeared as revenue deficit, committed expenditure, off-budget borrowing, contingent liabilities and Article 293 borrowing constraints.

Thus, Kerala’s White Papers reveal both transparency and failure. They show a state repeatedly capable of diagnosing its fiscal crisis, but less capable of transforming that diagnosis into lasting institutional correction. The lesson for 2026 is therefore clear: the present White Paper must not become another moment of political accusation followed by fiscal drift.

What the 2026 White Paper Says

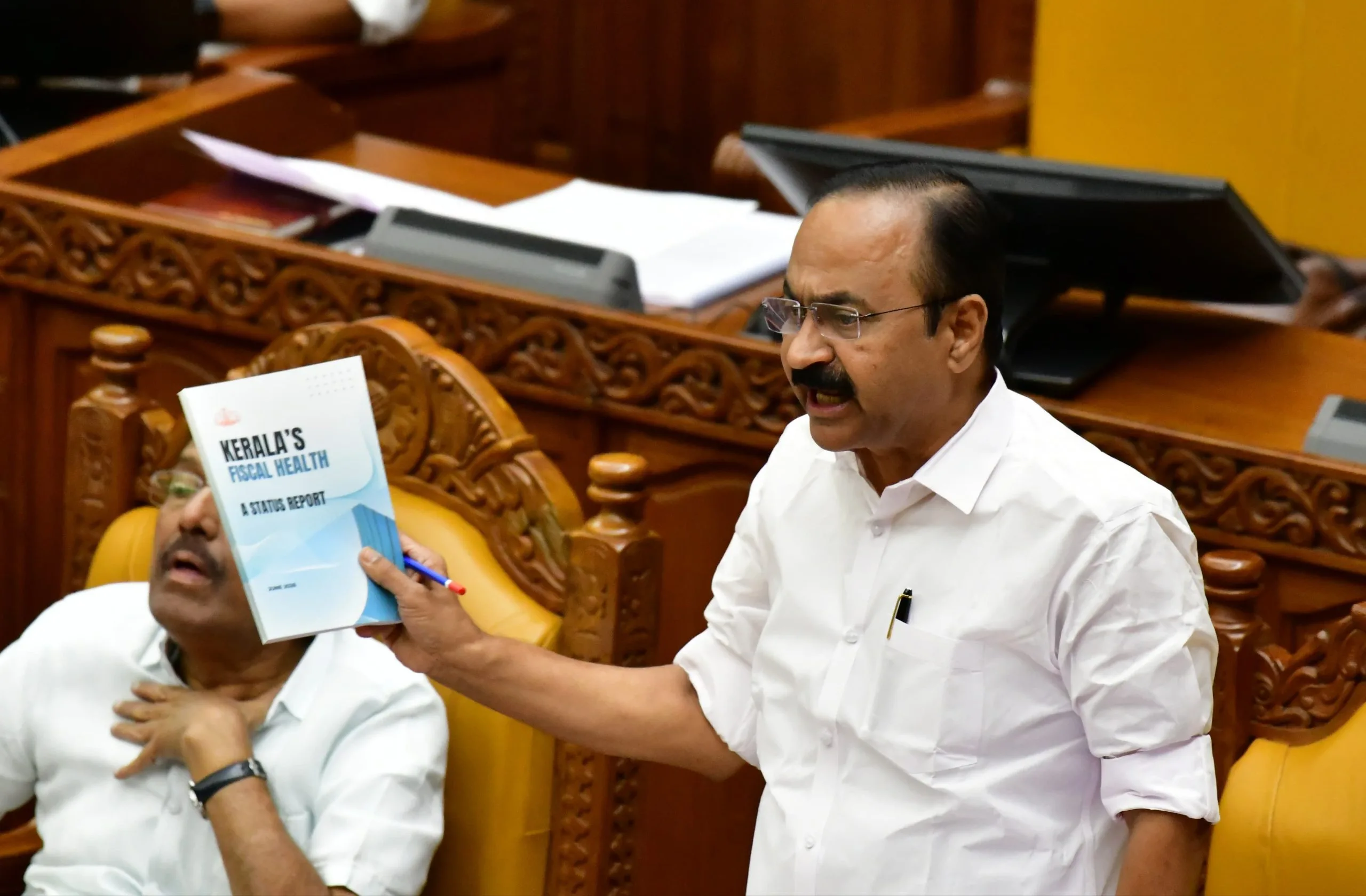

The 2026 White Paper, titled Kerala’s Fiscal Health: A Status Report, presents itself as a factual baseline rather than a forensic audit. Its stated aim is to show what the state receives, what it spends, what it owes and where the hidden pressures lie. Its scope is broad: revenue, expenditure, debt, treasury cash, off-budget entities, public sector enterprises, local governments, budgeting practices and allocations for marginalised communities. This makes the 2026 White Paper broader than earlier fiscal disclosure exercises because it includes cash management, arrears, off-budget liabilities, public enterprises, KIIFB, local governments and marginalised-community expenditure.

The central diagnosis is severe. Kerala’s outstanding liabilities are reported at around ₹5.07 lakh crore. Committed expenditure absorbs about 77% of total revenue receipts. Interest payments take away 20.9% of revenue receipts. Capital expenditure is only about 1.3% of GSDP. These figures show a state with very little fiscal room after meeting salaries, pensions, interest payments and routine obligations.

The report’s most important public finance warning is that Kerala has moved away from the principle of “borrow to invest, growth will repay.” Borrowing is not always bad. Borrowing for productive capital formation can be justified if it creates future income, employment, infrastructure and social returns. But borrowing for current expenditure, revenue deficits and debt servicing weakens the growth-generating capacity of debt. The White Paper argues that Kerala has increasingly fallen into this second pattern.

The section on treasury operations is especially revealing. It shows that the fiscal problem is not merely a matter of annual budget estimates. It appears daily in the treasury’s ability to make payments. Kerala has had to rely repeatedly on Ways and Means Advances and Overdraft from the Reserve Bank of India. The report states that in 2024–25 the treasury was in negative balance for 10 of 12 months. It also notes that treasury stress is not merely a cash management problem; it is the day-to-day operational expression of structural imbalance.

The report also identifies large inherited arrears. These include Dearness Allowance arrears, Dearness Relief arrears, contractor payments, bill discounting obligations and other deferred dues. Such arrears are not harmless accounting entries. They transfer fiscal stress to employees, pensioners, contractors, banks, welfare beneficiaries and future governments.

The White Paper is strongly critical of budget credibility. It argues that large deviations between budget estimates and actuals point to defective budgeting. State Own Tax Revenue has often fallen short of estimates, while committed expenditure remains difficult to compress. The report also criticises the manner in which plan expenditure is represented when KIIFB and some public sector spending are included in actuals but not in budget estimates.

KIIFB receives a major place in the White Paper. The report calls it a parallel fiscal authority, with its own borrowing programme, project pipeline and repayment obligations, but without the same legislative oversight and expenditure controls as the state budget. It reports an unmet KIIFB loan liability of around ₹21,000 crore and around ₹35,000 crore of already approved projects still requiring funding. It also says KIIFB’s cost of borrowing is about 1 to 1.5 percentage points higher than that of the state government. The report also raises serious questions about project distribution, noting that Kannur, Thiruvananthapuram and Ernakulam together account for nearly half of KIIFB allocations, without clear justification from human development or economic need indicators.

At the same time, the White Paper does not simply call for KIIFB’s abolition. It acknowledges that KIIFB was a bold institutional innovation, created organisational capacity, financed infrastructure and introduced project management and digital monitoring practices worth retaining. This is an important admission. The right conclusion is not to dismantle KIIFB, but to restructure it under transparent fiscal accounting, State Planning Board alignment, legislative reporting, project appraisal and social-return audit.

The report is equally critical of public sector enterprises. Kerala has a large number of state-level public enterprises, many of which are chronically loss-making. The accumulated loss of public enterprises has risen sharply, and KSRTC, KSSPL and KWA account for a large share of recent losses. The White Paper argues that social responsibility cannot become a cover for operational inefficiency. This is a valid point. But reform must distinguish between essential public utilities and non-strategic enterprises. Public ownership should be defended where it creates public value; it should be restructured where it merely drains public resources.

One of the most disturbing findings concerns development expenditure. Plan expenditure has stagnated and declined as a share of total expenditure. More seriously, expenditure for SC/ST/OBC and minority welfare has fallen as a share of total plan expenditure. This is where fiscal stress becomes a social justice issue. If fiscal correction reduces the resources available for marginalised communities, local governments, agriculture, education and social services, it will weaken the very foundations of the Kerala model.

The White Paper also places Kerala’s crisis within the changing structure of Indian fiscal federalism. The end of GST compensation, decline in Revenue Deficit grants, uncertainty in central transfers, tightening of borrowing limits and the treatment of off-budget borrowings under Article 293 have all reduced the fiscal flexibility of the state. This does not absolve Kerala of responsibility for internal reforms. But it shows that the fiscal crisis is shaped by both internal weaknesses and external constraints.

Critical Evaluation: What the White Paper Gets Right and What Requires Debate

The White Paper gets several things right. First, it widens the fiscal boundary. It does not restrict itself to the budget deficit; it includes off-budget entities, PSUs, arrears and liquidity stress. Second, it correctly identifies the problem of expenditure rigidity. Third, it highlights the poor quality of borrowing when debt finances current expenditure rather than capital formation. Fourth, it recognises the fiscal risks of KIIFB without dismissing its institutional achievements. Fifth, it shows how fiscal stress affects development expenditure and marginalised communities.

However, the White Paper must also be read critically. It should not become a political document that merely blames one government. Kerala’s fiscal stress is older than any one ministry. It stretches back at least to the period diagnosed by K. K. George in 1990. Successive governments expanded welfare commitments, postponed hard revenue decisions, tolerated weak public enterprise performance, underestimated future liabilities and relied on optimistic budget projections. Therefore, the White Paper should initiate a shared reform conversation, not a blame contest.

Second, the White Paper should not become a justification for narrow austerity. Kerala’s problem is not simply that it spends too much. It is also that it spends too rigidly, mobilises too little, invests too little in productive capacity and does not sufficiently measure the social return of public expenditure. Cutting expenditure blindly may reduce deficits temporarily but damage social foundations. A state like Kerala cannot solve its fiscal crisis by weakening public health, education, local governments or social justice commitments.

Third, the reform agenda should not over-romanticise private investment. Kerala needs private investment, cooperative investment, public investment and local-government-led economic development. But private capital will not automatically solve structural fiscal weakness. It requires infrastructure, regulatory clarity, skilled labour, power availability, land-use reform, ecological safeguards and political consensus. Growth is necessary, but growth without social justice will not be Kerala’s model.

Fourth, the White Paper should give greater importance to own-revenue mobilisation as a democratic political project. Kerala cannot permanently attribute its fiscal stress only to the Centre. Property taxation, non-tax revenue, tax compliance, user charges for commercial users, better public asset management and professional revenue administration require state-level reform. But revenue mobilisation must be progressive and socially defensible.

Fifth, the White Paper should deepen the discussion on decentralisation. Kerala’s planning tradition was built through local governments and people’s participation. If fiscal correction weakens local governments, Kerala will lose one of its strongest institutional assets. The state must protect untied funds, strengthen local revenue powers and make local governments partners in productive development.

Finally, the White Paper could have gone further in four areas. It needs a clearer framework for assessing the outcome quality of public expenditure—whether spending actually improves health, education, employment and productivity. It also needs an operational roadmap specifying what should be done in the first 100 days, the first year and the medium term. Equally important is the political economy of reform: how consensus will be built among employees, pensioners, local governments, welfare beneficiaries and taxpayers. Above all, Kerala needs a growth strategy with social justice, so that expansion of the productive base does not weaken labour rights, ecological safeguards or democratic decentralisation.

What Must Be Done?

Kerala needs a new public finance compact, sequenced across three-time horizons. In the immediate term, the government should publish a comprehensive public balance sheet covering direct debt, off-budget liabilities, guarantees, PSU exposure, deferred payments, arrears and KIIFB-related obligations. In the short to medium term, it should strengthen own-revenue mobilisation, restructure loss-making public enterprises and reform KIIFB. In the long term, Kerala must rebuild its productive base through employment-intensive growth, decentralised development and a fairer fiscal federal settlement.

Second, Kerala should adopt a modified golden rule of borrowing. Borrowing for routine revenue expenditure must be reduced. Borrowing for capital formation, climate resilience, public health, education, water security and employment-generating infrastructure should be permitted, but only with clear appraisal and repayment plans.

Third, KIIFB should be retained but restructured. It should not function as a parallel fiscal authority or parallel planning channel. It should become a transparent development-finance institution aligned with State Planning Board priorities, legislative scrutiny and social-return evaluation.

Fourth, public sector enterprises require differentiated reform. Essential utilities should remain accessible and affordable, but operational inefficiency must be addressed. Non-strategic and chronically unviable enterprises should face restructuring, merger, closure or professional turnaround.

Fifth, Kerala must protect development expenditure. Fiscal consolidation should not fall on SC/ST/OBC/minority welfare, local governments, agriculture, education and health. The quality of expenditure must improve, but social justice cannot become the casualty of fiscal correction.

Sixth, Kerala must rebuild its productive base. The state needs employment-intensive growth in tourism, health services, higher education, food processing, care economy, green industries, logistics, digital services, cooperative enterprises and local economic development. Fiscal sustainability ultimately depends on productive expansion.

Finally, fiscal reform must be democratic. Employees, pensioners, local governments, public enterprises, opposition parties, civil society, investors and citizens must be part of the conversation. Kerala’s crisis cannot be solved by technocracy alone. It requires political honesty and social negotiation.

Conclusion

The 2026 White Paper has opened the books. That is important. But opening the books is only the beginning. Kerala has seen White Papers before. They diagnosed fiscal stress, but did not produce lasting structural correction. The challenge now is to ensure that this White Paper does not become another document in the archive of warnings.

Kerala does not have to choose between welfare and fiscal responsibility. It must choose both. It must defend the Kerala model by reforming the fiscal foundations on which that model rests. The future lies neither in fiscal romanticism nor in harsh austerity, but in transparent developmental finance, accountable public institutions, productive growth and renewed social justice.

The real test of the White Paper will not be how strongly it criticises the past. The real test will be whether it helps Kerala build a fiscally credible, socially just and developmentally ambitious future.

References

George, K. K. (1990). Kerala’s fiscal crisis: A diagnosis. Economic and Political Weekly, 25(37), 2097–2105.

Government of Kerala. (2001). Revised budget speech 2001–02. Government of Kerala.

Government of Kerala. (2011). White paper on state finances. Finance Department, Government of Kerala.

Government of Kerala. (2016). White paper on state finances. Finance Department, Government of Kerala.

Government of Kerala. (2026). Kerala’s fiscal health: A status report. Finance Department, Government of Kerala.

Featured Image: Chief Minister V D Satheesan tabling ‘Kerala’s Fiscal Health: A Status Report’ in the Assembly on 05-06-2026. Image Courtesy: South First

Jos Chathukulam is a Professor of Political Economy and Director of the Centre for Rural Management (CRM), Kottayam, Kerala. His academic work focuses on public policy, decentralisation, public finance, local governance, development studies, and political economy in India, with a special emphasis on Kerala. Prof. Chathukulam has authored and edited several influential books and research papers, and has served as a policy advisor to governments and international agencies. He is widely recognised for his critical engagement with development paradigms and for advocating sustainable, people-centred alternatives in economic and governance practices.